How Much Money Do I Need To Emigrate To Canada

In the retirement series, I wrote about the Canada Pension Plan, RRSPs, Old Age Security, and other employment pension plans.

Taking it a step further, I want to address a question I've often asked myself (and have been asked by others):

"How much money do I need to have saved up before I retire?"

"How can I retire at age 50, 55, 60, or 65 years old?"

"How much income will I need in retirement?" …

or more specifically: "How much money do I need to retire in Canada?"

These, of course, are important questions!

As you grow older, you start to wonder if you're putting aside enough money for retirement and if your retirement nest egg will hold up when you finally do retire.

While I do not have all the answers, I'll take a stab at providing an answer that hopefully gets you started on the road to arriving at the "magic number" or "multiple" that works for you.

Retirement Income Calculation – Rules of Thumb

When it comes to income required in retirement in Canada, there are several rules of thumb or schools of thought out there. If you are looking for a definite answer to put your mind at rest, you may be disappointed.

In fact, the one thing everyone readily agrees to is that when it comes to retirement income, it is not "black and white" and there is no 100% consensus.

Popular rules of thumb include:

Rule 1: 4% Withdrawal Rate

The 4% withdrawal rule infers that you build up a retirement portfolio that provides a certain amount of income to you per annum at a 4% or so withdrawal rate. A 4% withdrawal rate is often referred to as a "safe" withdrawal rate.

For example, say you have figured out that you need $40,000 per year in retirement. Using a withdrawal rate of 4%, you should have a minimum of $1 million in retirement savings before you retire.

⇒ $40,000 ⁄ 4% = $1,000,000

This rule of thumb works whether you plan to retire early at 35 or go the conventional route and retire at 65 years or later. It's the strategy often utilized by many "early retirement" enthusiasts or the movement popularly referred to as "FIRE" – Financial Independence/Retire Early.

Note: For earlier retirement plans, consider that you will not be receiving a government pension or retirement benefits until later in life and adjust your income needs accordingly.

The general idea behind the funds lasting you for life is based on historical market returns. If we assume your investment portfolio generates approximately 7% annually in long-term returns, then real returns of approximately 4% are expected after accounting for inflation (assuming an inflation rate of 3%).

Essentially, a 4% withdrawal rate assumes your investment portfolio is not highly conservative (i.e. you are invested in a good proportion of stocks/equities).

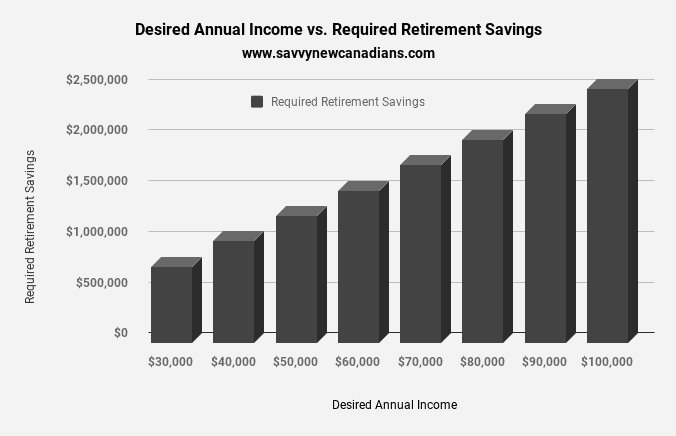

Rule 2: Desired Annual Retirement Income x 25

This rule follows the 4% withdrawal rate rule. They are pretty much the same, but this is easier to calculate for those who would rather not dabble in fractional math. It infers that in order to meet your income needs in retirement, you want to have at least 25 x your desired annual retirement income.

For example, say you estimate that your expenses per year in retirement are $40,000. You would be expected to save up a minimum of $1 million in retirement savings.

⇒ $40,000 x 25 = $1,000,000

Related: The Complete Guide to Retirement Income in Canada

Rule 3: 70% of Working Income (or more)

This rule estimates that you will need between 70% and 100% of your pre-retirement income in retirement: 70% if you are typical and do not have a mortgage, and up to 100% if you are still paying a hefty mortgage plus other atypical expenses while retired.

The idea behind this rule is that your expenses are generally expected to be lower in retirement: no mortgage payments, no longer need to save for retirement, kids are financially dependent, etc. After computing this amount, you can then proceed to calculate how much you need (lump-sum) by going back to Rule 1 or 2.

For example, assume you earn $100,000 per year before retiring. Using the 70% rule, you will need approximately $70,000 ($100,000 x 70%) in annual income to maintain your lifestyle in retirement. Going back to Rule 2, it implies you need:

⇒ $70,000 x 25 ⇒ $1.75 million in retirement.

I think the 70% rule is a fairly liberal estimate of retirement income needs (barring exceptional circumstances). A survey conducted by Sunlife and released in 2016, shows that Canadian retirees were on average living on 62% of their pre-retirement income.

Rule 4: Pre-Retirement Income x Multiples of 10 to 14

This rule suggests that you can calculate how much you need to save for retirement by multiplying your income just before retirement by a number between 10 and 14.

For example, say your income before retirement was $100,000/year. Following this rule, you should accumulate at least (depending on which multiple you're working with):

- Multiple of 10: $100,000 x 10 = $1 million

- Multiple of 11: $100,000 x 11 = $1.1 million

- Multiple of 12: $100,000 x 12 = $1.2 million

- Multiple of 13: $100,000 x 13 = $1.3 million

- Multiple of 14: $100,000 x 14 = $1.4 million … during your working years.

Rules 3 and 4 implicitly assume that you are using the income earned during your highest income-earning years as the basis of your calculation. This means that if you are a younger person in an entry-level position (i.e. low starting salary) who is looking at retiring early, calculations using these approaches will not work for you in the longer term.

Related: CPP vs. OAS: How Do They Compare?

Estimating Your Retirement Income Needs in Canada

The income available to you during your retirement years (distribution phase) will depend largely on how much you were able to set aside during your working years (accumulation phase), plus other available government and employment benefits.

Steps to estimating or calculating your retirement income needs include:

A. How much income do you expect to live on per year?

You can choose to compute this amount using different strategies – for example, by using the 70% pre-retirement income rule, or by simply looking at the lifestyle you envisage living in retirement and estimating what your expenses will add up to (including taxes).

Note: In your calculations, if looking at your current lifestyle and expenses, remember to eliminate expenses that may no longer be relevant in retirement such as mortgage payments, cost of commuting to work, childcare expenses; RRSP, CPP, and EI payments, etc. And, remember to add new expenses that may crop up such as travel expenses, hobbies, health issues, and so on.

B. How much government benefit do you expect to receive?

If you have lived and worked in Canada before retirement, you can expect to receive Old Age Security (OAS) and Canada Pension Plan (CPP) benefits.

The amount you receive will generally depend on how long you have lived in Canada (for OAS), how much you have contributed to the plan, and for how long (for CPP).

The maximum monthly OAS payable in 2021 (October to December quarter) is $635.26 for a total of $7,623.12 per year, while the maximum CPP was $1,203.75 for a total of $14,445 per year (2021).

Most people will get less than the maximum amount. For example, the average monthly CPP benefit paid as of June 2021 was $714.21 (41% less than the maximum amount payable at the time).

For individuals who immigrated to Canada in their adult years (like me), the total government pension they will be eligible for will be significantly reduced.

Using the 2021 maximum government pension amounts as an example, total payouts from this source to a single senior was:

$7,623.12 (OAS) + $14,445 (CPP) = $22,068.12 per year

C. How much do you need to save up?

To calculate this amount on an annual basis, you will need to subtract expected government pensions from the annual expenses you calculated in Step A , and then multiply the remainder by 25 (or divide by 4%).

For example, a couple who estimate their annual retirement income needs to be $70,000 will need to save:

| Annual expenses in retirement from age 65 (couple) | $70,000 |

| Deduct Total Government Pensions expected (couple) a | -$30,895 |

| Income Withdrawn from Savings/Year b | $39,105 |

| How Much Do You Need To Save For Retirement? c | $977,625 |

a. Most individuals will not get the full government pension amount from OAS and CPP. The amount here reflects 70% of the maximum CPP amount for a couple in 2021 i.e. (70% x $22,068.12) (x 2) – moderately conservative estimate.

b. Line 1 minus line 2

c. Derived by multiplying the annual income withdrawn by 25 (i.e. $39,105 x 25) or dividing by a 4% withdrawal rate (i.e. $39,105 / 4%). The result is the same for both formulas.

As shown in the table above, government pensions offset some of the savings required by the couple pre-retirement. The more government pension they qualify for, the less money required in their investment portfolio.

Additionally, if one or both partners have a defined benefit pension, it will further lower the amount of savings required to meet their desired retirement income.

Overall, to fund their preferred retirement lifestyle, the couple in the scenario above will need about $1 million in their retirement nest egg.

Related: CPP and OAS Benefits for Surviving Spouse and Children

What Can Change Your Retirement Income Needs?

Calculating your income needs in retirement is not an exact science. Life happens and it may leave your retirement plan in tatters. Some possibilities include:

- Health issues that cause you to retire earlier than planned or which result in higher-than-expected medical bills early in retirement

- Financially dependent kids in retirement

- Divorce

- Significant mortgage payments

- Run-away inflation or a market crash, and much more.

If for one reason or the other, you are unable to save enough money for retirement at age 60, or 65, or earlier depending on what your plans were initially, the following strategies may be useful in managing your "savings/income gap":

1. Work for longer and delay government pension till later: Working for a few more years and/or delaying when you start receiving OAS/CPP can significantly increase your eligible payouts down the road.

2. Semi-retire and work part-time: Every year you delay dipping into your retirement nest egg means more money to spend in the future.

3. Start saving aggressively: The earlier you start saving, the better for you. Time is the game-changer when it comes to the returns you are able to earn on your investment portfolio. If you are running out of time, you will need to put aside more funds more often.

4. Consider adjusting your retirement lifestyle expectations and spending less: If you have run out of time to build an adequate retirement portfolio to pay for the lifestyle you desire, you may have no choice but to take out less money from your savings and live accordingly.

5. Downsize and sell your home: You can consider beefing up your retirement savings by downsizing and selling your home so as to utilize the equity you have built up over the years. Alternatively, you may consider taking out a home equity line of credit (HELOC) or a reverse mortgage.

6. Other Government safety nets: If your income in retirement puts you in the low-income bracket (as specified by the government on an annual basis), you may qualify for additional government benefits, including the Guaranteed Income Supplement (GIS) or the Allowance.

Some resources that may come in handy as you plan for retirement include those provided by the Canadian Life and Health Insurance Association and this Retirement Calculator.

START INVESTING: Lower your investment fees with Canada's most popular online wealth manager (robo-advisor), Wealthsimple. Our readers get a $75 cash bonus when they open an account. Get started here!

Other Great Retirement Investing Posts:

- Wealthsimple Review: Invest on Autopilot and Save on Fees

- How To Generate Retirement Income From Your RRSP

- How To Generate Retirement Income From Your LIRA

- A Complete Guide To Simplified Investing in Canada

- The Ultimate Pre-Retirement Checklist For Canadians

- 5 Reasons to Delay Collecting CPP

- How To Save For Retirement in Canada

Closing Thoughts

When it comes to your retirement planning in Canada, starting early is the key. Compounding interest is your best friend, and it's better to be over-prepared than under-prepared.

So, do you feel you are on track with your retirement savings/planning? What amount do you feel you would need in retirement? Leave answers in the comment section below.

How Much Money Do I Need To Emigrate To Canada

Source: https://www.savvynewcanadians.com/money-needed-in-retirement/

Posted by: reillyaceir1939.blogspot.com

0 Response to "How Much Money Do I Need To Emigrate To Canada"

Post a Comment